The building products industry has been subject to persisting high levels of mergers and acquisitions (M&A) activity for the past several years. According to multiple reports, that activity is expected to continue into 2024. It could have big implications for the building products and construction industries.

“We continue to believe fundamentally that residential new construction and repair and remodel are going to be good markets,” says Scott Lavie, managing director of Renovo Capital, who is quoted in a building products report published by middle-market investment bank Brown Gibbons Lang & Company (BGLC). “In the short term, we think that the trepidation that exists today based on economic uncertainties probably has impacted the financing market and valuations. Long term, we’ll get through that.”

“We continue to believe fundamentally that residential new construction and repair and remodel are going to be good markets,” says Scott Lavie, managing director of Renovo Capital, who is quoted in a building products report published by middle-market investment bank Brown Gibbons Lang & Company (BGLC). “In the short term, we think that the trepidation that exists today based on economic uncertainties probably has impacted the financing market and valuations. Long term, we’ll get through that.”

In its report, BGLC acknowledges a recent dip in the pace of M&As in the building products industry, but, like Lavie, is more bullish on long-term prospects, calling its outlook “favorable”—which is the sentiment throughout the investment community.

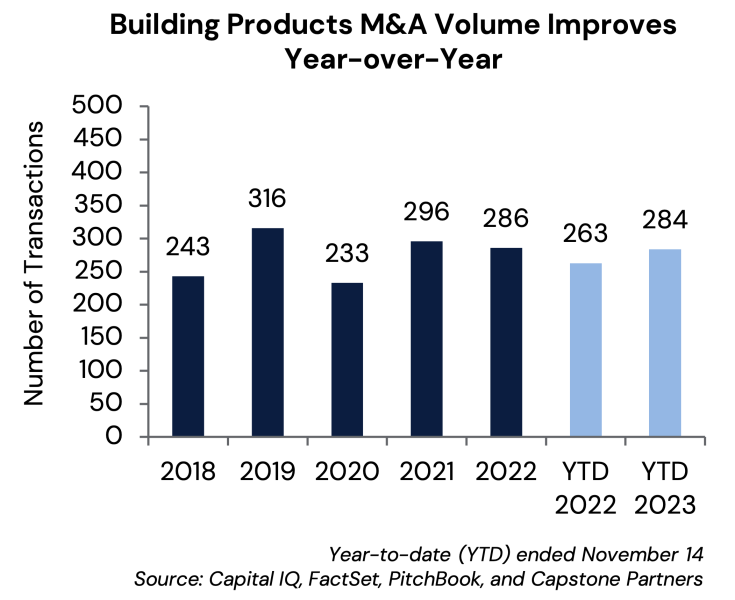

A separate December 2023 report on the building products space from investment bank Capstone Partners reads, “M&A activity is expected to remain robust through year-end and into 2024 as strategics and financial buyers continue to eye acquisition opportunities.”

Building Product M&A Opportunities: Consolidation

While building product M&As are expected to continue in 2024, lingering economic and industry challenges are altering the strategy with which deals are approached and closed.

“Many potential acquisition candidates in the building products space have exhibited highly volatile performance over the past several years,” says Matt Kaufman, managing director of Validor Capital, who was also quoted in BGLC’s report. “The primary challenge is evaluating the sustainability of their most recent performance.”

Inflation, persisting supply chain issues, labor availability and costs, these are all issues dampening short-term outlooks.

“Being a supplier to the industry, our biggest challenge is restoring profitability margin after struggling through the past couple of years of volatility,” Lavie of Renovo Capital says. “With current supply chain stability and raw material prices normalizing, our customers all want cost reductions.”

But investors still see opportunities in the building products space. Chris Ayala, managing director of Drum Capital Management, and Matt Fish, managing director of consulting firm Stax, who are both quoted in BGLC’s report, agree that consolidation is one of those opportunities.

“There are many smaller service businesses that performed well the last several years that could be rolled up and put into a consolidation platform that fall outside of the business model of the larger strategic acquirers,” Ayala says. “Those might be really nice opportunities for us as we think through the future.”

Fish explains that one of the biggest current drivers of consolidation, at least for his clients, is the prospect of mitigating current and future supply chain issues.

“Product producers are looking to consolidate their supply chains,” he says. “One of the areas where we expect outsized consolidation is service businesses like roofing and residential HVAC with many of the larger industry participants undergoing a roll-up strategy to expand geographically and leverage the increased scale to benefit from synergies.”

A report from Capstone Partners explains the appetite for consolidation in building products. It reads, “The fragmentation of the sector has created a favorable environment for buy-and-build strategies, with many sponsors adding smaller tuck-ins to portfolio holdings at low buy-in multiples.”

In layman's terms, “buy and build” refers to a company expanding its operational abilities and bandwidth through the acquisition of platform companies with desired expertise. An example would be Masonite’s recent acquisition of Fleetwood Aluminum Products, which the company purchased as part of its operational expansion strategy.

Of the acquisition, Howard Heckes, president and CEO of Masonite, said, "This is the second acquisition we have completed in 2023 as part of our Doors That Do More strategy to expand our product portfolio and address new and non-traditional segments of the market with innovative and differentiated door systems.”

Building Product M&A Opportunities: Regional Strengths

How well building products perform is, of course, tied to the construction industry’s overall performance, which is why investors working in the building products space also tend to keep a close eye on construction at large. In doing so, they’ve identified areas of potential growth as well as potential problem areas.

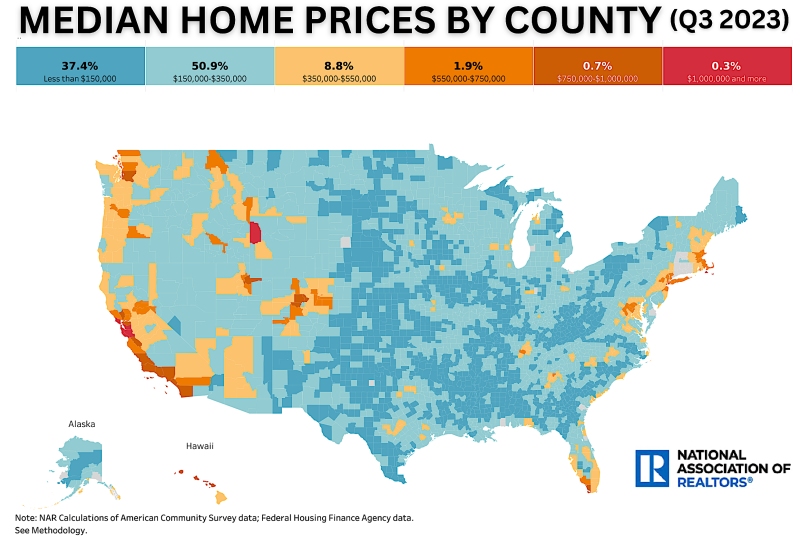

In BGLC’s report, Validor Capital Managing Director Matt Kaufman is quoted as saying, ”While there may be some variation in outcomes across different regions, we are particularly optimistic about the Southeast, Florida, Texas, and select Western states.” He explains his strong demand outlook, at least in part, as a result of “the emergence of millennials as first-time homebuyers and the current deficit in single and multi-family housing resulting from underinvestment over the last decade.”

Last updated March 7, 2024.

Drum Capital Management’s Ayala agrees with Kaufman, saying, “There are obvious places such as Texas and the Southeast … where prices are still reasonable for homes, where the cost of living continues to be low, and where people have an opportunity to work in professional environments on a remote basis.” He adds, “I think those markets continue to be strong.”

Image: National Association of Realtors

One area where investors are a bit more bearish is California.

“We are seeing an exodus of people and business from California,” says Lavie of Renovo Capital. “The tech sector has been hammered; a lot of people losing jobs, and equity values of companies being negatively impacted. These negative economic consequences that are occurring in some of the major tech cities will likely cause specific declines.”

Why Building Product M&As Matter

The implications of building product industry M&As for purchasers, and specifically residential construction professionals, are myriad. An acquisition can signal an expansion of product lines, like with Masonite’s acquisition of Fleetwood, as mentioned above, or with PGT Innovations' full acquisition of Eco Enterprises (a process that began in 2021), which PGT President and CEO Jeff Jackson explained was a means increase production capacity and diversify product lines.

“Since acquiring ownership in Eco, we’ve been able to utilize this vertical integration to service the glass needs for some of our other brands,” Jackson said. “We’re very excited to reach the finalization of this purchase as it will allow us to further serve high growth markets in which we operate.”

Building product industry M&As can also result in brand consolidation, in which one or multiple brands may effectively disappear altogether. An example is Woodgrain's acquisition of Huttig Building Product. Woodgrain acquired Huttig in 2022 but didn’t fully absorb the company (and discontinue its brand) until April 2023.

These M&As can lead to expanded service areas (while giving residential construction professionals insight into the regions these companies are betting big on)—like when the Indiana-based Ambassador Supply acquired Florida-based Hitek Truss to help the company better service the Southeastern US—or help bring a foreign brand into the US market—like when Atlas Holdings sold Erickson Construction, provider of residential framing materials and services, to Toyko-based Asahi Kasei Group. Not to mention, many of these deals involve investor dollars—and specifically private-equity investment—with which come unique possibilities for change that could impact the industry at large.

To help keep residential construction professionals more up to date with the biggest mergers and acquisitions as well as the expansions affecting the residential building products industry, we've tracked down and consolidated dozens of announcements made since 2017 and organized them in the below timeline for easy access and exploration. The timeline will be updated periodically, so continue checking back.

Add new comment